Ensemble methods

are commonly used to boost predictive accuracy by combining the

predictions of multiple machine learning models. The traditional wisdom

has been to combine so-called “weak” learners. However, a more modern

approach is to create an ensemble of a well-chosen collection of strong

yet diverse models.

Building powerful ensemble models has many parallels with building

successful human teams in business, science, politics, and sports. Each

team member makes a significant contribution and individual weaknesses

and biases are offset by the strengths of other members.

The simplest kind of ensemble is the unweighted average of the

predictions of the models that form a model library. For example, if a

model library includes three models for an interval target (as shown in

the following figure), the unweighted average would entail dividing the

sum of the predicted values of the three candidate models by three. In

an unweighted average, each model takes the same weight when an ensemble

model is built.

Averaging predictions to form ensemble models.

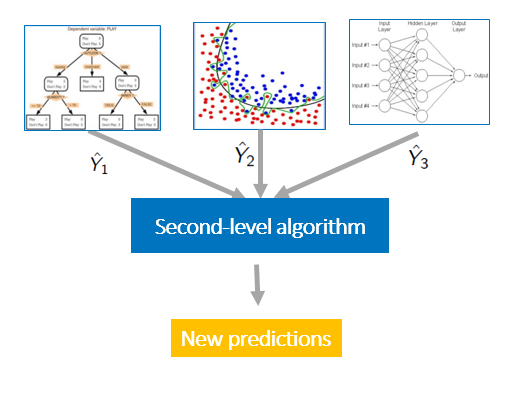

More generally, you can think about using weighted averages.

For example, you might believe that some of the models are better or

more accurate and you want to manually assign higher weights to them.

But an even better approach might be to estimate these weights more

intelligently by using another layer of learning algorithm. This

approach is called model stacking. Model stacking is an efficient ensemble method in which the

predictions, generated by using various machine learning algorithms, are

used as inputs in a second-layer learning algorithm. This second-layer

algorithm is trained to optimally combine the model predictions to form a

new set of predictions. For example, when linear regression is used as

second-layer modeling, it estimates these weights by minimizing the

least square errors. However, the second-layer modeling is not

restricted to only linear models; the relationship between the

predictors can be more complex, opening the door to employing other

machine learning algorithms.

Model stacking uses a second-level algorithm to estimate prediction weights in the ensemble model.

Meet me at O'Reilly

Join me at the O’Reilly Artificial Intelligence

Conference April 30-May 2 to learn more about combining traditional

statistical techniques with machine learning algorithms. Don’t miss

these SAS presentations: Long-Term Time Series Forecasting With Recurrent Neural Networks Mustafa Kabul, Senior Data Scientist, SAS

May 1 | 11:55 a.m. – 12:35 p.m. Improving Wildlife Conservation With Artificial Intelligence Mary Beth Ainsworth, AI and Language Analytics Strategist, SAS

May 1 | 2:35 – 3:15 p.m. Well-Established Statistical Techniques + Modern Machine Learning Algorithms Funda Gunes, Senior Machine Learning Developer, SAS

May 2 | 1:45 – 2:25 p.m. Online and Active Learning for Recommender Systems Jorge Silva, Principal Machine Learning Developer, SAS

May 2 | 4:50 – 5:30 p.m.

Winning data science competitions with ensemble modeling

Ensemble modeling and model stacking are especially popular in data

science competitions, in which a sponsor posts a training set (which

includes labels) and a test set (which does not include labels) and

issues a global challenge to produce the best predictions of the test

set for a specified performance criterion. The winning teams almost

always use ensemble models instead of a single fine-tuned model. Often

individual teams develop their own ensemble models in the early stages

of the competition, and then join their forces in the later stages.

On the popular data science competition site Kaggle

you can explore numerous winning solutions through its discussion

forums to get a flavor of the state of the art. Another popular data

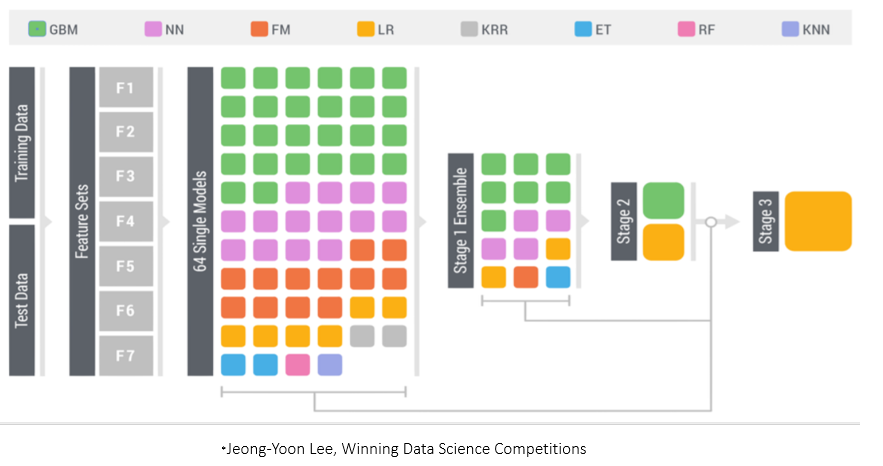

science competition is the KDD Cup. The following figure shows the winning solution for the 2015 competition, which used a three-stage stacked modeling approach.

The figure shows that a diverse set of 64 single models were used to

build the model library. These models are trained by using various

machine learning algorithms. For example, the green boxes represent

gradient boosting models (GBM), pink boxes represent neural network

models (NN), and orange boxes represent factorization machines models

(FM). You can see that there are multiple gradient boosting models in

the model library; they probably vary in their use of different

hyperparameter settings and/or feature sets.

At stage 1, the predictions from these 64 models are used as inputs

to train 15 new models, again by using various machine learning

algorithms. At stage 2 (ensemble stacking), the predictions from the 15

stage 1 models are used as inputs to train two models by using gradient

boosting and linear regression. At stage 3 ensemble stacking (the final

stage), the predictions of the two models from stage 2 are used as

inputs in a logistic regression (LR) model to form the final ensemble.

In order to build a powerful predictive model like the one that was used to win the 2015 KDD Cup, building a diverse set of initial models plays an important role! There are various ways to enhance diversity such as using:

Different training algorithms.

Different hyperparameter settings.

Different feature subsets.

Different training sets.

A simple way to enhance diversity is to train models by using

different machine learning algorithms. For example, adding a

factorization model to a set of tree-based models (such as random forest

and gradient boosting) provides a nice diversity because a

factorization model is trained very differently than decision tree

models are trained. For the same machine learning algorithm, you can

enhance diversity by using different hyperparameter settings and subsets

of variables. If you have many features, one efficient method is to

choose subsets of the variables by simple random sampling. Choosing

subsets of variables could be done in more principled fashion that is

based on some computed measure of importance which introduces the large

and difficult problem of feature selection.

In addition to using various machine learning training algorithms and

hyperparameter settings, the KDD Cup solution shown above uses seven

different feature sets (F1-F7) to further enhance the diversity.

Another simple way to create diversity is to generate various versions

of the training data. This can be done by bagging and cross validation.

How to avoid overfitting stacked ensemble models

Overfitting is an omnipresent concern in building predictive models,

and every data scientist needs to be equipped with tools to deal with

it. An overfitting model is complex enough to perfectly fit the training

data, but it generalizes very poorly for a new data set. Overfitting is

an especially big problem in model stacking, because so many predictors

that all predict the same target are combined. Overfitting is partially

caused by this collinearity between the predictors.

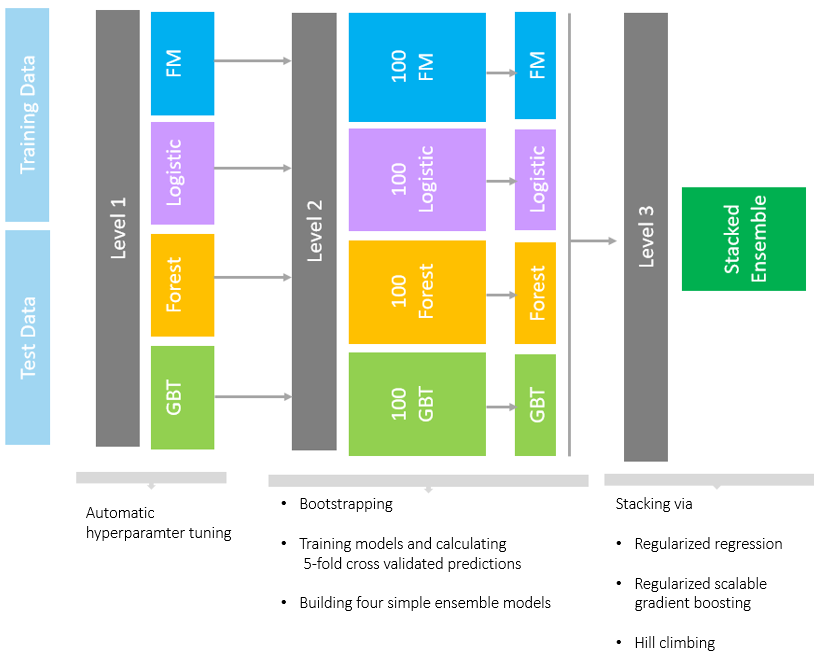

The most efficient techniques for training models (especially during

the stacking stages) include using cross validation and some form of

regularization. To learn how we used these techniques to build stacked

ensemble models, see our recent SAS Global Forum paper, "Stacked Ensemble Models for Improved Prediction Accuracy." That

paper also shows how you can generate a diverse set of models by

various methods (such as forests, gradient boosted decision trees,

factorization machines, and logistic regression) and then combine them

with stacked ensemble techniques such regularized regression methods,

gradient boosting, and hill climbing methods.

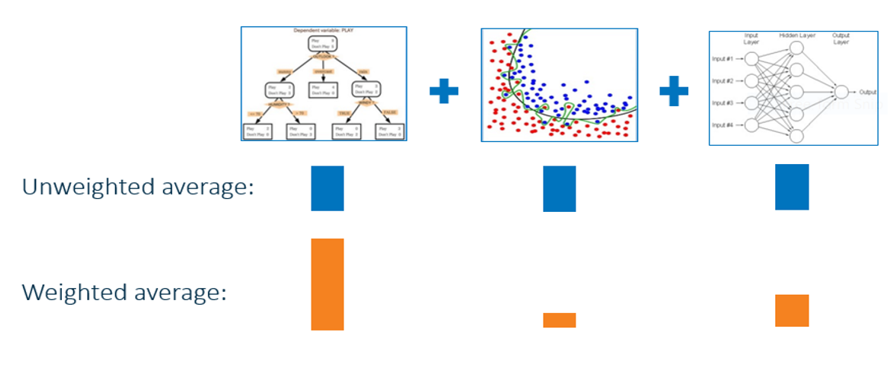

The following image provides a simple summary of our ensemble

approach. The complete model building approach is explained in detail

in the paper. A computationally intense process such as this benefits

greatly by running in a distributed execution environment offered in the

SAS® Viya platform by using SAS® Visual Data Mining and Machine Learning.

A diverse set of models combined with stacked ensemble techniques.

Applying stacked models to real-world big data problems can produce

greater prediction accuracy and robustness than do individual models.

The model stacking approach is powerful and compelling enough to alter

your initial data mining mindset from finding the single best model to

finding a collection of really good complementary models.

Of course, this method does involve additional cost both because you

need to train a large number of models and because you need to use cross

validation to avoid overfitting. However, SAS Viya provides a modern

environment that enables you to efficiently handle this computational

expense and manage an ensemble workflow by using parallel computation in

a distributed framework. To learn more, check out our paper, "Stacked Ensemble Models for Improved Prediction Accuracy," and read the SAS Visual Data Mining and Machine Learning documentation.

Presented at Data Science Salon in Dallas by Brian Kursar, Vice President and Chief Data Scientist at Toyota Connected.

Data

is everywhere: in our digital footprint, in our financial system, and

in our cities, down to the very cars we drive. Vehicles have become

increasingly smart, and are now rich sources of data from which to

derive valuable insights about customer behavior. We were thrilled to be

joined by Brian Kursar, Vice President and Chief Data Scientist at

Toyota Connected at the Data Science Salon in Dallas. He imagines a

future where cars continue to add value to their drivers far after they

leave the dealership. Here’s the transcript, from his fascinating talk.

I’m

very excited to talk to everyone about Toyota Connected! First off let

me just ask who here has heard of Toyota Connected. No, not

Toyota — Toyota Connected. Wow, very very cool! For those of you who

don’t know, Toyota Connected is a brand new company. We are about three

minutes away from the corporate office. And we are a for-profit company.

What we do is we are the arm for data science and data engineering for

Toyota. We are a start-up and a start-up in the sense that we truly are a

startup — we have about 200 engineers, we work in a different building,

our culture is completely different than Toyota Motors in North America

but we are powered by Toyota. We have a lot of the backing by the

parent company and that really allows us to do a lot of things [that

are] very innovative [in] a very different type of culture where we’re

empowering our team with the ability to make decisions and to follow

through in those decisions. As I mentioned, it’s a completely different

office and if you walk into our office you will notice we have a

dog-friendly policy and we have free lunches for everyone. As a matter

of fact one of my favorite things about Toyota Connected is they

actually label the vegan soups which is a something that makes me very

happy.

Let

me talk a little bit about where we see things and where Toyota

Connected fits in. We see that the car is really an essential piece of

the internet of everything. You really start out with the Toyota

Connected car. And what is that? Behind the scenes every Toyota

Connected car coming out since July 2017 is able to transmit sensors of

data representing various things such as whether or not the windows are

down, GPS, speedometer, odometer, steering angle. But all of these we do

only with the consent of the customer. These vehicles actually are dead

when you go to the dealership. But we will actually walk you through

some of the various use cases for our safety connect program and this is

what I’ll be talking about today. However we only enable it once the

customer understands what data we’re collecting and how we’re using that

data to create new and exciting services for them. The

average customer drives about 48 minutes per day — about 500+ unique

data points are generated every 200 milliseconds and that really comes

out to about 7.2 million data points per connected vehicle per day

[that’s] A LOT OF DATA! Petabytes of data!What do we do

with it? First and foremost as I mentioned earlier [we] write data

services that drive customer satisfaction, we’re looking to create new

and exciting services that make driving safer, more convenient, and fun.

Next we’ll use that data to really derive new insights to make our

products better.

In

the very short time that Toyota Connected has been around, for two

years now — we’ve had a number of milestones. In April 2017, we worked

with the folks in Tour to connect [with] Japan on a project called Japan

Taxi which I’ll be talking about in a moment. The connected car went

live in July of 2017 and that was for the model year Camry 2018. We then

looked at actually using that data in what we call a car share pilot on

the Island of Hawaii with a company that does distribution for our

vehicles there. And then finally we went live with the car share pilot

we now called Hui as well as going forward with Avis to be able to

connect the vehicles in their rental problem transactions. Japan Taxi

was our first really deep dive into the connected car because this was

done before vehicles in the U.S. were connected. Actually this was done

before vehicles in the US or Japan were connected. For this pilot we

teamed up with TRI. For those who don’t know, TRI is the research arm of

Toyota that focuses on the autonomous vehicle. This was an opportunity

to really work with them to collect data and provide them data from

actual people driving taxis in Japan. With this project, we used special

aftermarket devices for eight hours a day every day — and actually it’s

still going now — we are collecting the data from these trips. If you

look here, this is actually a really quick video of our application that

we created. In this application, each dot represents a vehicle and all

this is collected in real time — you can actually drill in to one of the

vehicles and then see the vehicles driving. This one here is driving

late at night (our morning, night in Japan) on the streets.

What do we use this for?

This is actually what we’re doing: leveraging machine learning, optic

recognition and then providing that and those videos to Tour, the

research institute, to be able to take what they’re finding and create

their own algorithms to improve the autonomous vehicle. Another thing we

do is outside of research, we look at new ways to provide new services

for our customers. One of the things is we’re developing a driver score

that’s gonna be live probably in the next four to six months. Actually

Demuth’s working on it — he’s sitting in the back there and he can talk

to you more about that if you’re interested. Here’s what a driving score

is: we have a set of metrics or rules that Nitsa provides and to enable

us to take what we call CANbus data or data that’s coming out of the

vehicle and derive insights and scores on different types of events.

Primarily we’re looking at longitudinal and lateral g-force, you’re

looking at the location, speed, and then how much you’re applying on

brake pressure. To give you an example [let’s] really drill down into

four trips. The Green will represent what we call smooth driving. I mean

not going past the speed limit, you’re not doing the harsh braking,

you’re not having any harsh right turns or left turns or over speeding.

The red there is what we would call harsh braking. Then you got that

maroon which I can’t don’t think you see well in here, which represents

over speeding. Above the line there you’ve got the horsepower

acceleration, and here I don’t think we have any hard left turns. What

does this look like? They’re actually drilling down even further, so

here’s one of those trips, and as you can see here the green just drills

down. The green shows that the person currently driving here is driving

37.96 miles per hour, the location at that point is 40 miles per hour

therefore it’s green. There’s no harsh braking, there’s no longitude or

added lateral g-force popping out, and as you can see for the most part

this person is driving smooth. Just about 15 seconds later you can

actually see that this person is now speeding. The speed limit there is

30 miles per hour and this person is going 49.56 miles per hour. Keep in

mind every one of these dots is a single second. Four seconds later

this customer actually hits the brakes really hard, and now you’re able

to see that red line or the red circle which shows harsh braking.

That’s nice information — what are we doing with that?

We’re able to provide the customer with driving tips. These are tips

that will help them understand their overall trip score, what their

acceleration is, what their speed is. We are able to now take these tips

and show them how they can get better miles per gallon. We’re also able

to allow them to say, this is my data and I’m going to actually do

something with it. They can take this data and they can send it out to a

another service called Toyota Information Insurance Management

Services. If they are a good driver, they can send this data to

different insurance companies and have them bid for discounts for that

customer. US models starting with Camry 2018 which came out in July have

these sensors. Now these sensors are actually dead at the

dealership — you have to actually go through a walkthrough where the

dealer talks to you about what the data is collected how it’s being

collected and then you can actually opt-in. We don’t we don’t collect

the data unless you opt-in, but it’s for the most recent Camry, the

upcoming rav4, upcoming Avalon, and I think there’s a handful of Lexus

vehicles as well. Fleet is one of our number one customers because the

fleet customers want to know things that are a lot more detailed in

terms of vehicle location. They want to understand such things as, are

the windows open or closed, has the car been in a collision, what is the

fuel level.

A

lot of things that I mentioned earlier with the Avis project that’s

actually gone live for a fleet to be able to understand the health of

the vehicle and to cut down on the time that they’re spending on the

checkout process. It’s not in blockchain but we do have a data store

that the data is being saved in, yes. Question: hey why do you call it a G Force because what you’re really measuring is stress, strain, and shear forces?

G forces are typically used as a nomenclature when you have a force

large enough to make it feel like a percentage of gravity — at least

half a G. Right, so the transfer of the G Force is from kinetic energy

to potential energy. That’s how we are able to understand our harsh

cornering, harsh braking as well. It’s not just the brake pressure at

all, true, but I think that’s the way that we look at it. There is a

guideline and they actually consider it as g-force. You can actually get

it after the trip is completed, we do this at a trip level. We do have

the potential to provide it in real time but we actually only provide

that at the end of the trip for at least the next version that will be

coming out.

The

next type of service that we provide is what we call collision

detection. Very similarly we’re looking at the longitudinal lateral

g-force, the acceleration, brake pressure. Here I’d like to say that you

know the data really tells a story and this is just an example — where

we have the longitudinal, lateral, and vertical g-force; so that’s the

X, Y, & Z axis here. And here you can see the acceleration — a red

line here and so as the customer is driving and they accelerate you can

actually see that in that line coming down here and it goes to about

there as they stop. Now the moment you see that transfer of energy — you

can see that it’s right about here — and that’s actually what we’re

able to use to understand collision notifications. The problem is

that — this person was lucky because the airbag was triggered — the way

the sensors are set up on the vehicle as well as how we are measuring

that, we were able to understand front collisions and we’ve been doing

that for many, many years. But the problem is that the airbag does not

go off when you have a rear-end collision or side collision or if you

were to flip over and find yourself in the bottom of a ditch. And so

because of that we’ve realized that we have to now really start looking

at the data a little bit differently and understand that some of the

airbag sensors that yes, they do trigger a notification and they will

call the paramedics — these are things that are not enough to ensure the

safety of our customers.

What

we’ve been doing now, is looking at classifying crashes into three

different buckets, and then also looking at how do we eliminate some of

the false positives. For instance, this is the area right here where

you’re going between five and eight point five in the magnitude of the

g-force and that’s where we traditionally will have airbags deployed. If

you then go and look at areas that are not being looked at — these are

things that we mentioned, you know the high to medium/low speed crashes

where it is a side impact, where it is a rear impact, where the cars

flipped over. Now those are the areas where we need to be able to

understand but also eliminate the false positive. Harsh braking and

harsh cornering are absolutely false positives. What about other things

like hitting a shopping cart? Well that’s not so bad. What about going

over a speed bump? Well that’s also not a collision. We teamed up with a

number of companies to pull in data so that we can actually compare

some of the things like video data, data where they’ve actually done

crash tests — and then pass those through our models to be able to

derive kind of what we call the area of opportunity or the areas where

we can now provide newer and better services than were available before.

Different

drivers who drive in the same car have different styles — like my wife

and I, we share one of those Camrys. In the future though I think we

will have head units [that] are very much like Netflix, where you can

actually use a profile and based on that profile it’ll be able to keep

your settings from a temperature perspective, what radio stations you

listen to, what are the places that you like to eat, or do

recommendations. However, we don’t have that today in our vehicles.

Today

we do use cloud, and we only use cloud for what we’re doing today in

terms of metadata management. When this application was created, we had

specifications coming from our product engineers that really defined all

the data. It’s telemetry data, it’s all structured, we have data

dictionaries on everything to help the data scientists understand what

it is. One of the things that we are doing as a new company, we are

really starting on our journey to data science. I was actually hired to

build out a data science practice for the company. We pulled all of our

data scientists to gather and really talk about the things that are

possible with this data — we d this on regular basis.

There’s

a lot of things that we see from a services perspective that we can

provide to the customer. In fact, we only do this to provide services

for the customer. There’s no reason to use the data unless we can make

our products better and we can provide these new types of services for

our customers. For instance, in this case we envision that when our

collision notification is ready to be deployed — this is something that

we’ll be calling you over the telephone and having someone saying “hey

we noticed that there’s been a collision, are you okay?” — if someone

doesn’t answer we dispatch a unit to that location. Or being able to

essentially have a notification pop-up on their phone, saying do you

need to send assistance? There’s going to be low impact use cases where

someone got rear-ended, we still want to be there for our customer. I

think that there was a statistic that one of our data scientists

provided me, which was, one out of every ten collisions that ends in a

fatality could have been prevented if we had the ability to get someone

dispatched quicker. For me, that’s something that I’m definitely looking

towards seeing what we can do on our side to make a difference there

and to make our vehicles safer.

We’ve

talked a lot about what we do as a company. From a company culture

perspective, we are absolutely focused on bringing in the best talent.

We are really connected and are committed to helping folks understand

what we are all about, what we do and entice anyone that might be

interested to work for us. We have a number of open positions and please

come see me if you’re interested :).

I

bought a Toyota Camry mostly because I wanted to understand the full

experience, what is it that our dealerships are truly saying to the

customer and just so I could understand and be able to talk about it as a

Toyota customer. I was actually very impressed with the way they walked

me through everything and how they showed us these are things that you

can do to enable these services and this is the data we collect and the

reality is that when my wife is driving the car of course I’m gonna

opt-in. Why? Because I want safety connect. Why? Because if she’s ever

in an accident they’re there for her. These are services that I think

people are going to opt-in for because they provide a genuine value add

to the vehicle. I bought the vehicle also because it has what they call

smart sense to be able to understand if someone’s to the right or left

to me before I’m making a lane change. All of this really comes down to

safety features. From a scale perspective we definitely recognize that

the cost to be able to provide these services is something that we’re

grappling with. We’re absolutely looking at ways to optimize

algorithms — how we’re storing the data, when how much we’re storing, to

really only hold the value add attributes to be able to do these

algorithms and provide these services. Thank you very much!

We’ve

got a lineup of equally impressive speakers from companies like Viacom,

Netflix, Buzzfeed, Forbes, Verizon, Nielsen, Comcast, Bloomberg, Uber,

Google and many, many more.

Github: https://github.com/pengpaiSH/Kaggle_NCFM

Step1. Download dataset from https://www.kaggle.com/c/the-nature-conservancy-fisheries-monitoring/data

Step2. Use split_train_val.py to split the labed data into training

and validation. Usually, 80% for training and 20% for validation is a

good start.

Step3. Use train.py to train a Inception_V3 network. The best model and its weights will be saved as "weights.h5".

Step4. Use predict.py to predict labels for testing images and

generating the submission file "submit.csv". Note that such submission

results in a 50% ranking in the leaderboard.

Step5. In order to improve our ranking, we use data augmentation for

testing images. The intuition behind is similar to multi-crops, which

makes use of voting ideas. predict_average_augmentation.py implements

such idea and results in a 10% ranking (Public Score: 1.09) in the

leaderboard.

Step 6. Note that there is still plenty of room for improvement. For

example, we could split data into defferent training and valition data

by cross-validation, e.g. k-fold. Then we train k models based on these

splitted data. We average the predictions output by the k models as the

final submission. This strategy will result a 5% ranking (Public Score:

1.02) in the leaderboard. We will leave the implementation as a practice

for readers :)

Step 7: if you wanna to improve ranking further, object detection is your next direction!

Update and Note: In order to use flow_from_directory(), you should create a folder named test_stg1 and put the original test_stg1 inside it.

Feature engineering, feature selection, and model evaluation

Like most problems in life, there are several potential approaches to a Kaggle competition:

Lock yourself away from the outside world and work in isolation

I

recommend against the “lone genius” path, not only because it’s

exceedingly lonely, but also because you will miss out on the most

important part of a Kaggle competition: learning from other data scientists.

If you work by yourself, you end up relying on the same old methods

while the rest of the world adopts more efficient and accurate

techniques.

As

a concrete example, I recently have been dependent on the random forest

model, automatically applying it to any supervised machine learning

task. This competition finally made me realize that although the random

forest is a decent starting model, everyone else has moved on to the

superior gradient boosting machine.

The other extreme approach is also limiting:

2. Copy one of the leader’s scripts (called “kernels” on Kaggle), run it, and shoot up the leaderboard without writing a single line of code

I

also don’t recommend the “copy and paste” approach, not because I’m

against using other’s code (with proper attribution), but because you

are still limiting your chances to learn. Instead, what I do recommend

is a hybrid approach: read what others have done, understand and even

use their code, and build on other’s work with your own ideas. Then,

release your code to the public so others can do the same process,

expanding the collective knowledge of the community.

In

the second part of this series about competing in a Kaggle machine

learning competition, we will walk through improving on our initial

submission that we developed in the first part.

The major results documented in this article are:

An increase in ROC AUC from a baseline of 0.678 to 0.779

Over 1000 places gained on the leaderboard

Feature engineering to go from 122 features to 1465

Feature selection to reduce the final number of features to 342

Decision to use a gradient boosting machine learning model

We

will walk through how we achieve these results — covering a number of

major ideas in machine learning and building on other’s code where

applicable. We’ll focus on three crucial steps of any machine learning

project:

Feature engineering

Feature selection

Model evaluation

To

get the most out of this post, you’ll want to follow the Python

notebooks on Kaggle (which will be linked to as they come up). These

notebooks can be run on Kaggle without downloading anything on your

computer so there’s little barrier to entry! I’ll hit the major points

at a high-level in this article, with the full details in the notebooks.

Brief Recap

If you’re new to the competition, I highly recommend starting with this article and this notebook to get up to speed.

The Home Credit Default Risk competition

on Kaggle is a standard machine learning classification problem. Given a

dataset of historical loans, along with clients’ socioeconomic and

financial information, our task is to build a model that can predict the

probability of a client defaulting on a loan.

In the first part of this series,

we went through the basics of the problem, explored the data, tried

some feature engineering, and established a baseline model. Using a

random forest and only one of the seven data tables, we scored a 0.678 ROC AUC (Receiver Operating Characteristic Area Under the Curve) on the public leaderboard. (The public leaderboard is calculated with only 20% of the test data and the final standings usually change significantly.)

To

improve our score, in this article and a series of accompanying

notebooks on Kaggle, we will concentrate primarily on feature

engineering and then on feature selection. Generally, the largest benefit relative to time invested

in a machine learning problem will come in the feature engineering

stage. Before we even start trying to build a better model, we need to

focus on using all of the data in the most effective manner!

Notes on the Current State of Machine Learning

Much

of this article will seem exploratory (or maybe even arbitrary) and I

don’t claim to have made the best decisions! There are a lot of knobs to

tune in machine learning, and often the only approach is to try out

different combinations until we find the one that works best. Machine

learning is more empirical than theoretical and relies on testing rather

than working from first principles or a set of hard rules.

In a great blog post, Pete Warden

explained that machine learning is a little like banging on the side of

the TV until it works. This is perfectly acceptable as long as we write

down the exact “bangs” we made on the TV and the result each time.

Then, we can analyze the choices we made, look for any patterns to

influence future decisions, and find which method works the best.

My

goal with this series is to get others involved with machine learning,

put my methods out there for feedback, and document my work so I can

remember what I did for the next time! Any comments or questions, here

or on Kaggle, are much appreciated.

Feature Engineering

Feature engineering

is the process of creating new features from existing data. The

objective is to build useful features that can help our model learn the

relationship between the information in a dataset and a given target. In

many cases — including this problem — the data is spread across multiple tables.

Because a machine learning model must be trained with a single table,

feature engineering requires us to summarize all of the data in one

table.

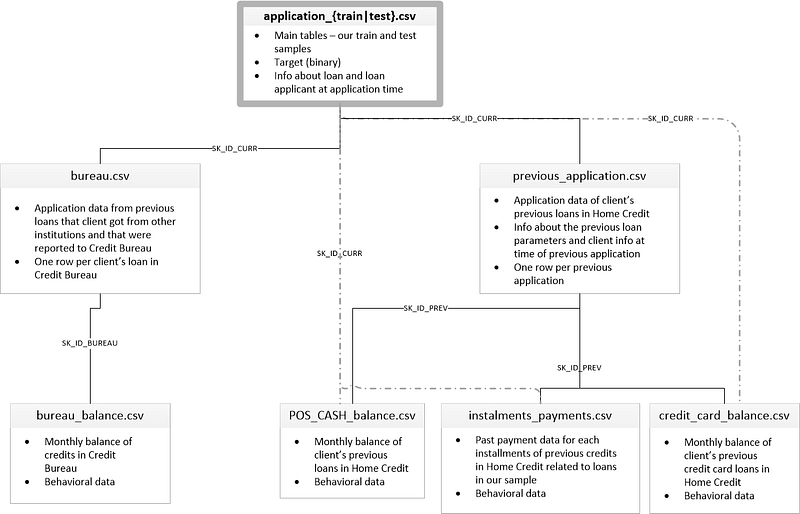

This competition has a total of 7 data files.

In the first part, we used only a single source of data, the main file

with socioeconomic information about each client and characteristics of

the loan application. We will call this table app.(For those used to Pandas, a table is just a dataframe).

Main training dataframe

We can tell this is the training data because it includes the label, TARGET. A TARGET value of 1 indicates a loan which was not repaid.

The app dataframe is tidy structured data: there is one row for every observation — a client’s application for a loan — with the columns containing the features

(also known as the explanatory or predictor variables). Each client’s

application — which we will just call a “client” — has a single row in

this dataframe identified by the SK_ID_CURR.

Because each client has a unique row in this dataframe, it is the

parent of all the other tables in the dataset as indicated by this

diagram showing how the tables are related:

When

we make our features, we want to add them to this main dataframe. At

the end of feature engineering, each client will still have only a

single row, but with many more columns capturing information from the

other data tables.

The six other tables contain information about clients’ previous loans, both with Home Credit (the institution running the competition), and other credit agencies. For example, here is the bureau dataframe, containing client’s previous loans at other financial institutions:

bureau dataframe, a child of app

This dataframe is a child table of the parentapp: for each client (identified by SK_ID_CURR)

in the parent, there may be many observations in the child. These rows

correspond to multiple previous loans for a single client. The bureau dataframe in turn is the parent of the bureau_balance dataframe where we have monthly information for each previous loan.

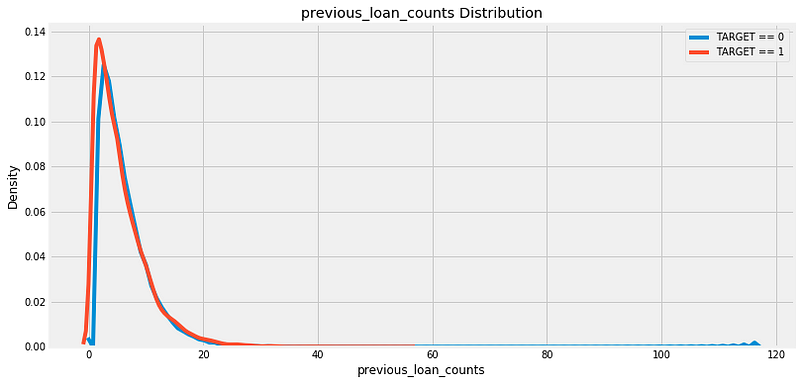

Let’s

look at an example of creating a new feature from a child dataframe:

the count of the number of previous loans for each client at other

institutions. Even though I wrote a post about automated feature engineering, for this article we will stick to doing it by hand. The first Kaggle notebook to look at is here: is a comprehensive guide to manual feature engineering.

Calculating this one feature requires grouping (using groupby)the bureau dataframe by the client id, calculating an aggregation statistic (using agg with count) and then merging (using merge)

the resulting table with the main dataframe. This means that for each

client, we are gathering up all of their previous loans and counting the

total number. Here it is in Python:

app dataframe with new feature in second column

Now

our model can use the information of the number of previous loans as a

predictor for whether a client will repay a loan. To inspect the new

variable, we can make a kernel density estimate (kde) plot.

This shows the distribution of a single variable and can be thought of

as a smoothed histogram. To see if the distribution of this feature

varies based on whether the client repaid her/his loan, we can color the

kde by the value of the TARGET:

There does not appear to be much of a difference in the distribution, although the peak of the TARGET==1 distribution is slightly to the left of the TARGET==0

distribution. This could indicate clients who did not repay the loan

tend to have had fewer previous loans at other institutions. Based on my

extremely limited domain knowledge, this relationship would make sense!

Generally,

we do not know whether a feature will be useful in a model until we

build the model and test it. Therefore, our approach is to build as many

features as possible, and then keep only those that are the most

relevant. “Most relevant” does not have a strict definition, but we will

see some ways we can try to measure this in the feature selection

section.

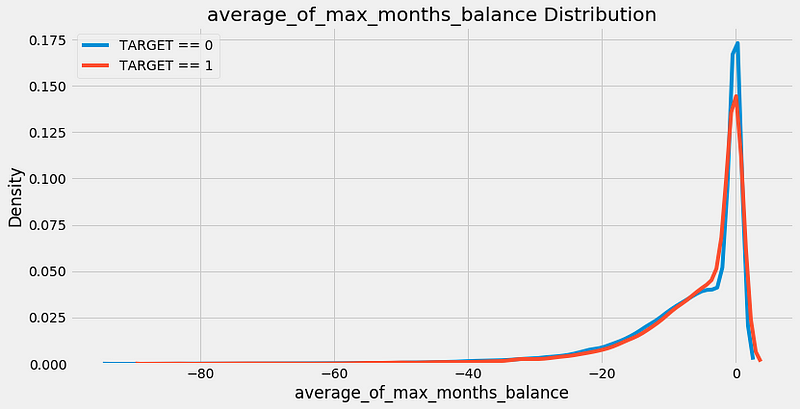

Now let’s look at capturing information not from a direct child of the app dataframe, but from a child of a child of app! The bureau_balance dataframe contains monthly information about each previous loan. This is a child of the bureau

dataframe so to get this information into the main dataframe, we will

have to do two groupbys and aggregates: first by the loan id (SK_ID_BUREAU) and then by the client id.

As an example, if we want to calculate for each client the average of the max number of MONTHS_BALANCE for each previous loan in the bureau_balance dataframe, we can do this:

app dataframe with new feature in second column

Distribution of new feature

This

was a lot of code for a single feature, and you can easily imagine that

the manual feature engineering process gets tedious after a few

features! That’s why we want to write functions that take these

individual steps and repeat them for us on each dataframe.

Instead of repeating code over and over, we put it into a function — called refactoring — and

then call the function every time we want to perform the same

operation. Writing functions saves us time and allows for more

reproducible workflows because it will execute the same actions in

exactly the same way every time.

Below

is a function based on the above steps that can be used on any child

dataframe to compute aggregation statistics on the numeric columns. It

first groups the columns by a grouping variable (such as the client id),

calculates the mean, max, min, sum of

each of these columns, renames the columns, and returns the resulting

dataframe. We can then merge this dataframe with the main app data.

(Half

of the lines of code for this function is documentation. Writing proper

docstrings is crucial not only for others to understand our code, but

so we can understand our own code when we come back to it!)

To see this in action, refer to the notebook, but clearly we can see this will save us a lot of work, especially with 6 children dataframes to process.

This

function handles the numeric variables, but that still leaves the

categorical variables. Categorical variables, often represented as

strings, can only take on a limited number of values (in contrast to

continuous variables which can be any numeric value). Machine learning

models cannot handle string data types, so we have to find a way to capture the information in these variables in a numeric form.

As an example of a categorical variable, the bureau table has a column called CREDIT_ACTIVE that has the status of each previous loan:

Two columns of the bureau dataframe showing a categorical variable (CREDIT_ACTIVE)

We

can represent this data in a numeric form by counting the number of

each type of loan that each client has had. Moreover, we can calculate

the normalized count of each loan type by dividing the count for one

particular type of loan by the total count. We end up with this:

Categorical CREDIT_ACTIVE features after processing

Now

these categorical features can be passed into a machine learning model.

The idea is that we capture not only the number of each type of

previous loan, but also the relative frequency of that type of loan. As

before, we don’t actually know whether these new features will be useful

and the only way to say for sure is to make the features and then test

them in a model!

Rather

than doing this by hand for every child dataframe, we again can write a

function to calculate the counts of categorical variables for us.

Initially, I developed a really complicated method for doing this

involving pivot tables and all sorts of aggregations, but then I saw

other code where someone had done the same thing in about two lines

using one-hot encoding. I promptly discarded my hours of work and used

this version of the function instead!

This function once again saves us massive amounts of time and allows us to apply the same exact steps to every dataframe.

Once

we write these two functions, we use them to pull all the data from the

seven separate files into one single training (and one testing

dataframe). If you want to see this implemented, you can look at the first and second manual engineering notebooks. Here’s a sample of the final data:

Using information from all seven tables, we end up with a grand total of 1465 features! (From an original 122).

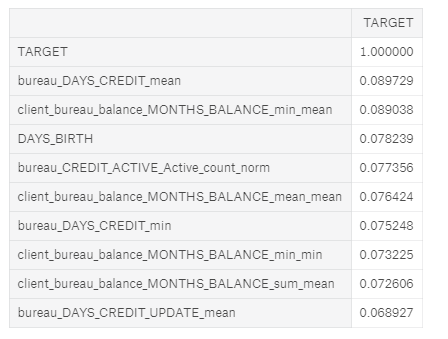

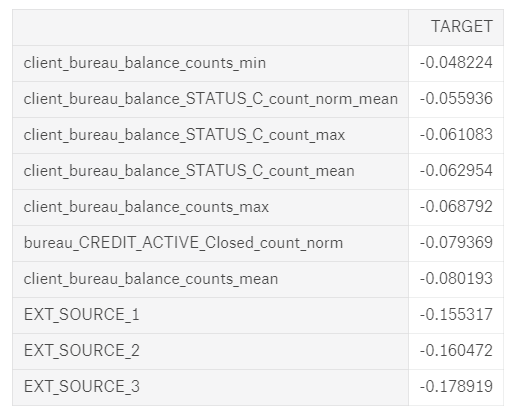

How do we know if any of these features are helpful? One method is to calculate the Pearson correlation coefficient between the variables and the TARGET.

This is a relatively crude measure of importance, but it can serve as

an approximation of which variables are related to a client’s ability to

repay a loan. Below are the most correlated variables with the TARGET:

Most Positive (left) and Negative (right) correlated variables with the TARGET

The EXT_SOURCE_

variables were from the original features, but some of the variables we

created are among the top correlations. However, we want to avoid

reading too much into these numbers. Anytime we make a ton of features,

we can run into the multiple comparisons problem:

the more comparisons we make — in this case correlations with the

target — the more likely some of them are to be large due to random

noise. With correlations this small, we need to be especially careful

when interpreting the numbers.

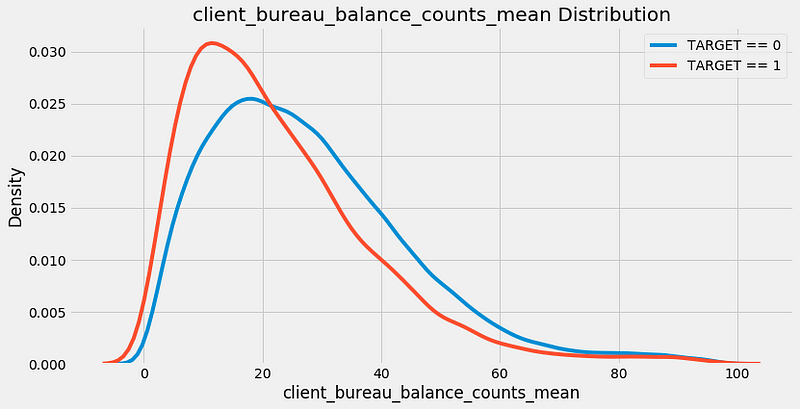

The most negatively correlated variable we made, client_bureau_balance_counts_mean, represents the average for each client of the count of the number of times a loan appeared in the bureau_balance data. In other words, it is the average number of monthly records per previous loan for each client. The kde plot is below:

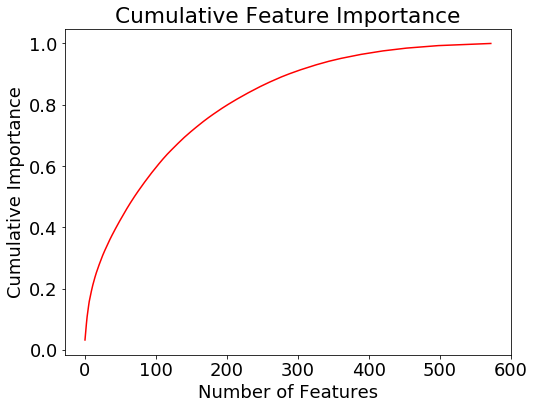

Now that we have 1465 features, we run into the problem of too many features! More menacingly, this is known as the curse of dimensionality, and it is addressed through the crucial step of feature selection.

Feature Selection

Too

many features can slow down training, make a model less interpretable,

and, most critically, reduce the model’s generalization performance on

the test set. When we have irrelevant features, these drown out the

important variables and as the number of features increases, the number

of data points needed for the model to learn the relationship between

the data and the target grows exponentially (curse of dimensionality explained).

After

going to all the work of making these features, we now have to select

only those that are “most important” or equivalently, discard those that

are irrelevant.

The next notebook to go through is here: a guide to feature selection which is fairly comprehensive although it still does not cover every possible method!

There are many ways to reduce the number of features, and here we will go through three methods:

Removing collinear variables

Removing variables with many missing values

Using feature importances to keep only “important” variables

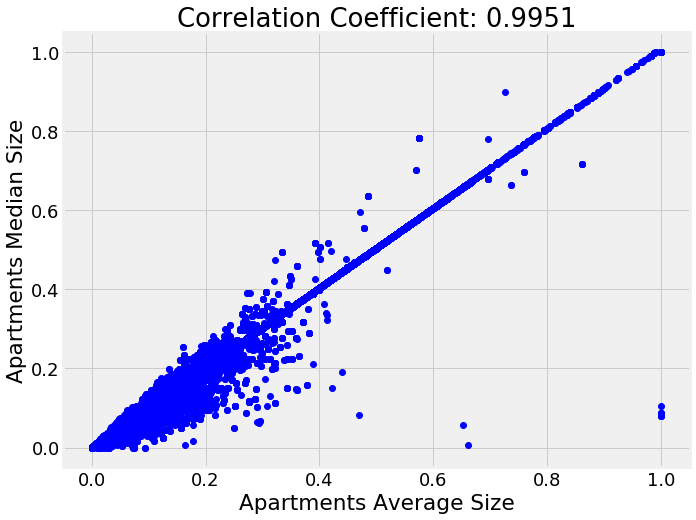

Remove Collinear Variables

Collinear variables

are variables that are highly correlated with one another. These

variables are redundant in the sense that we only need to keep one out

of each pair of collinear features in order to retain most of the

information in both. The definition of highly correlated can vary and

this is another of those numbers where there are no set rules! As an

example of collinear variables, here is a plot of the median apartment

size vs average apartment size:

To

identify highly correlated variables, we can calculate the correlation

of every variable in the data with every other variable (this is quite a

computationally expensive process)! Then we select the upper triangle

of the correlation matrix and remove one variable from every pair of

highly correlated variables based on a threshold. This is implemented in

code below:

In

this implementation, I use a correlation coefficient threshold of 0.9

to remove collinear variables. So, for each pair of features with a

correlation greater than 0.9, we remove one of the pair of features. Out of 1465 total features, this removes 583, indicating many of the variables we created were redundant.

Remove Missing Columns

Of

all the feature selection methods, this seems the most simple: just

eliminate any columns above a certain percentage of missing values.

However, even this operation brings in another choice to make, the threshold percentage of missing values for removing a column.

Moreover, some models, such as the Gradient Boosting Machine in LightGBM,

can handle missing values with no imputation and then we might not want

to remove any columns at all! However, because we’ll eventually test

several models requiring missing values to be imputed, we’ll remove any

columns with more than 75% missing values in either the training or

testing set.

This

threshold is not based on any theory or rule of thumb, rather it’s

based on trying several options and seeing which worked best in

practice. The most important point to remember when making these choices

is that they don’t have to be made once and then forgotten. They can be

revisited again later if the model is not performing as well as

expected. Just make sure to record the steps you took and the

performance metrics so you can see which works best!

Dropping columns with more than 75% missing values removes 19 columns from the data, leaving us with 863 features.

Feature Selection Using Feature Importances

The

last method we will use to select features is based on the results from

a machine learning model. With decision tree based classifiers, such as

ensembles of decision trees (random forests, extra trees, gradient

boosting machines), we can extract and use a metric called the feature

importances.

The technical details of this is complicated (it has to do with the reduction in impurity from including the feature

in the model), but we can use the relative importances to determine

which features are the most helpful to a model. We can also use the

feature importances to identify and remove the least helpful features to

the model, including any with 0 importance.

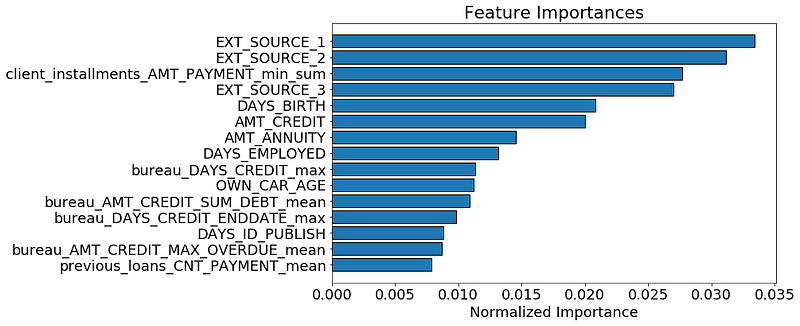

To find the feature importances, we will use a gradient boosting machine (GBM) from the LightGBM library.

The model is trained using early stopping with two training iterations

and the feature importances are averaged across the training runs to

reduce the variance.

Running this on the features identifies 308 features with 0.0 importance.

Removing

features with 0 importance is a pretty safe choice because these are

features that are literally never used for splitting a node in any of

the decision trees. Therefore, removing these features will have no

impact on the model results (at least for this particular model).

This

isn’t necessary for feature selection, but because we have the feature

importances, we can see which are the most relevant. To try and get an

idea of what the model considers to make a prediction, we can visualize

the top 15 most important features:

Top 15 most important features

We

see that a number of the features we built made it into the top 15

which should give us some confidence that all our hard work was

worthwhile! One of our features even made it into the top 5. This

feature, client_installments_AMT_PAYMENT_min_sum

represents the sum of the minimum installment payment for each client

of their previous loans at Home Credit. That is, for each client,it is

the sum of all the minimum payments they made on each of their previous

loans.

The

feature importance don’t tell us whether a lower value of this variable

corresponds to lower rates of default, it only lets us know that this

feature is useful for making splits of decision trees nodes. Feature

importances are useful, but they do not offer a completely clear interpretation of the model!

After

removing the 0 importance features, we have 536 features and another

choice to make. If we think we still have too many features, we can

start removing features that have a minimal amount of importance. In

this case, I continued with feature selection because I wanted to test

models besides the gbm that do not do as well with a large number of

features.

The

final feature selection step we do is to retain only the features

needed to account for 95% of the importance. According to the gradient

boosting machine, 342 features are enough to cover 95% of the

importance. The following plot shows the cumulative importance vs the

number of features.

Cumulative feature importance from the gradient boosting machine

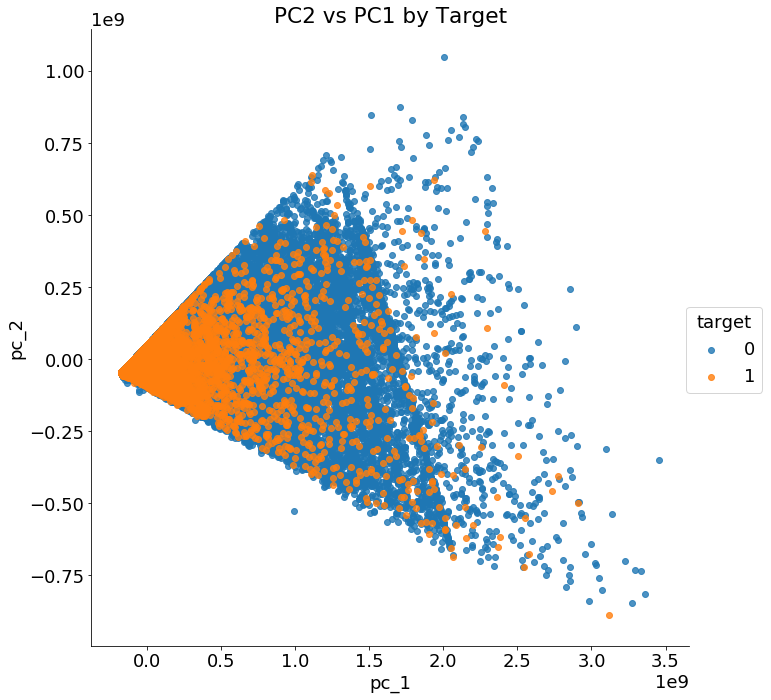

There are a number of other dimensionality reduction techniques we can use, such as principal components analysis (PCA).

This method is effective at reducing the number of dimensions, but it

also transforms the features to a lower-dimension feature space where

they have no physical representation, meaning that PCA features cannot

be interpreted. Moreover, PCA assumes the data is normally distributed,

which might not be a valid assumption for human-generated data. In the

notebook I show how to use pca, but don’t actually apply it to the data.

We can however use pca for visualizations. If we graph the first two principal components colored by the value of the TARGET , we get the following image:

First two principal components of the data

The

two classes are not cleanly separated with only two principal

components and clearly we need more than two features to identify

customers who will repay a loan versus those who will not.

Before moving on, we should record the feature selection steps we took so we remember them for future use:

Remove collinear variables with a correlation coefficient greater than 0.9: 583 features removed

Remove columns with more than 75% missing values: 19 features removed

Remove 0.0 importance features according to a GBM: 308 features removed

Keep only features needed for 95% of feature importance: 193 features removed

The final dataset has 342 features.

If

it seems like there are a few arbitrary choices made during feature

selection, that’s because there were! At a later point, we might want to

revisit some of these choices if we are not happy with our performance.

Fortunately, because we wrote functions and documented our decisions,

we can easily change some of the parameters and then reassess

performance.

Model

selection is one area where I relied heavily on the work of others. As

mentioned at the beginning of the post, prior to this competition, my

go-to model was the random forest. Very early on in this competition

though, it was clear from reading the notebooks of others that I would

need to implement some version of the gradient boosting machine in order

to compete. Nearly every submission at the top of the leaderboard on

Kaggle uses some variation (or multiple versions) of the Gradient

Boosting Machine. (Some of the libraries you might see used are LightGBM, CatBoost, and XGBoost.)

Over the past few weeks, I have read through a number of kernels (see here and here)

and now feel pretty confident deploying the Gradient Boosting Machine

using the LightGBM library (Scikit-Learn does have a GBM, but its not as

efficient or as accurate as other libraries). Nonetheless, mostly for

curiosity’s sake, I wanted to try several other methods to see just how

much is gained from the GBM. The code for this testing can be found on Kaggle here.

This

isn’t entirely a fair comparison because I was using mostly the default

hyperparameters in Scikit-Learn, but it should give us a first

approximation of the capabilities of several different models. Using the

dataset after applying all of the feature engineering and the feature

selection, below are the modeling results with the public leaderboard

scores. All of the models except for the LightGBM are built in

Scikit-Learn:

Logistic Regression = 0.768

Random Forest with 1000 trees = 0.708

Extra Trees with 1000 trees = 0.725

Gradient Boosting Machine in Scikit-Learn with 1000 trees = 0.761

Gradient Boosting Machine in LightGBM with 1000 trees = 0.779

Average of all Models = 0.771

It

turns out everyone else was right: the gradient boosting machine is the

way to go. It returns the best performance out of the box and has a

number of hyperparameters that we can adjust for even better scores.

That does not mean we should forget about other models, because

sometimes adding the predictions of multiple models together (called ensembling) can perform better than a single model by itself. In fact, many winners of Kaggle competitions used some form of ensembling in their final models.

We

didn’t spend too much time here on the models, but that is where our

focus will shift in the next notebooks and articles. Next we can work on

optimizing the best model, the gradient boosting machine, using

hyperparameter optimization. We may also look at averaging models

together or even stacking multiple models to make predictions. We might

even go back and redo feature engineering! The

most important points are that we need to keep experimenting to find

what works best, and we can read what others have done to try and build

on their work.

Conclusions

Important

character traits of being a data scientist are curiosity and admitting

you don’t know everything! From my place on the leaderboard, I clearly

don’t know the best approach to this problem, but I’m willing to keep

trying different things and learn from others. Kaggle

competitions are just toy problems, but that doesn’t prevent us from

using them to learn and practice concepts to apply to real projects.

In this article we covered a number of important machine learning topics:

Using feature engineering to construct new features from multiple related tables of information

Applying feature selection to remove irrelevant features

Evaluating several machine learning models for applicability to the task

After

going through all this work, we were able to improve our leaderboard

score from 0.678 to 0.779, in the process moving over a 1000 spots up

the leaderboard. Next, our focus will shift to optimizing our selected

algorithm, but we also won’t hesitate to revisit feature

engineering/selection.

If you want to stay up-to-date on my machine learning progress, you can check out my work on Kaggle:

the notebooks are coming a little faster than the articles at this

point! Feel free to get started on Kaggle using these notebooks and

start contributing to the community. I’ll be using this Kaggle

competition to explore a few interesting machine learning ideas such as Automated Feature Engineering and Bayesian Hyperparameter Optimization.

I plan on learning as much from this competition as possible, and I’m

looking forward to exploring and sharing these new techniques!

More generally, you can think about using weighted averages.

For example, you might believe that some of the models are better or

more accurate and you want to manually assign higher weights to them.

But an even better approach might be to estimate these weights more

intelligently by using another layer of learning algorithm. This

approach is called model stacking.

More generally, you can think about using weighted averages.

For example, you might believe that some of the models are better or

more accurate and you want to manually assign higher weights to them.

But an even better approach might be to estimate these weights more

intelligently by using another layer of learning algorithm. This

approach is called model stacking.